Dollaricide I

The Domestic Death of Our Currency System

Almost all of us in the United States, whether attentive to our infotainment journalists or not, are at least subconsciously aware of something terribly wrong lurking in our economy. Even if we naively believe that our politicians and the Federal Reserve can forever find new ways to kick the can down the road and avoid present payment for past financial sins, we somehow know that our basic assumptions about our finances will someday, perhaps soon, fail us all. Few are prepared for that in the manner of John Galt in his hidden Colorado valley (see “Atlas Shrugged” by Ayn Rand). Nonetheless we take comfort in the notion that, when the U.S. economic system hits the iceberg of intractable indebtedness, all of us will be in the same leaky lifeboat. Still, if we awaken to that which daily lurks below the surface, might we as individuals, families, and even a country, may be able to paddle to a less frigid end?

In following the work of several economic and financial analysts of international reputation (Patrick Barron, Godfrey Bloom, Emile Woolf, Alasdair Macleod et al) and trying to decipher their expertise into layman’s terms, I have found certain threads of commonality linking the U.S. economic missteps with a sea change in the international order we have known. Curiously my best current source of understanding what is happening now in America comes from a financial analyst in the United Kingdom,

. His latest, a private email presumably soon to be published on his Substack, reviews the mistakes and pitfalls of Great Britain in recent decades, all of which we, as loyal expatriates, seem to be mirroring.His column, “Monetary tinkering or real reform?” is quoted and commented on at length below. My second essay, Dollaricide II, will expand on this internationally based on work by Alasdair Macleod and a recent Aljazeera article cited in that next writing. I hope the thread can be followed by my readers, agreeable or not.

"Defenders of QE <quantitative easing after 2008> claimed that, whatever its dangers, it succeeded in saving many banks from the consequences of their own greed-driven prodigality: in particular, granting mortgages on hugely overvalued sub-prime properties; offering “liar loans” to borrowers without even rudimentary creditworthiness checks; and monetising the bubble into circulation by wrapping all this dross in parcels of financial instruments carrying Double-A status attached by conflicted rating-agencies, and then “selling” these junk bonds to the next institution in the suckers’ queue."

The above process shielded our financial elites from any consequences as they were massively enriched through selling these artificial assets to the populace at large via banks, investment funds, and retirement accounts to ‘recycle’’ these as new money disguised as further credit. With the collapse of this in 2008-2009 that fantasy wealth of the masses vanished. ‘Homeowners’ were foreclosed, and zombie business’ surviving on misallocated capital went under with the attendant loss of jobs.

"Critics of QE, on the other hand, don’t need the benefit of hindsight to see that the banks it saved from annihilation were unworthy of the money-showering measures applied by central banks to bail them out "

Nor have they become worthy; the pigs remain at the government’s fiscal trough which has been recycling the pigs’ own excrement for their foodstuff.

"The exhaustive money-printing and interest-rate suppression by central banks became the remedy-of-choice for any and every economic hiccup..an addiction"

One of the key features of addiction is tachyphylaxis, or the constant and accelerating need for more of the drug (free money) to satisfy the same inexhaustible hunger (a house of cards economy). Only an enlarged body of need could prevent an overdose that would put the economy into an intractable coma without means of resuscitation. But then….

"the pandemic struck and the <Federal Reserve>, with the tacit connivance of the Treasury, launched another spree of money-printing that enabled banks"...to shovel fiat currency into circulation for a host of distortive welfare benefits that " now constitute the norm in a society plagued by the dependency that those benefits have cultivated. "

Forty, to over Fifty, percent, depending on your information source, of the U.S. population is now dependent on some means of government funding, and cannot detoxify themselves. The symptoms of withdrawal (doing without big screen tv, the internet, larger than necessary automobiles, and constant attention to one’s cell phone) violate entitlements that have become First World unalienable rights.

"central bankers are trained to believe that changes in the money supply and inflation are unconnected."

This is the ironclad legacy of John Maynard Keynes, who carved into the stone fronts of our government buildings and the gray matter of our souls that production of goods and formation of capital don’t matter. All public good is contained solely in maintaining and enhancing demand through artificial production of demand (as thought desirable by the government rather than the free market) through creation of free money via untethered fiat currency and unlimited new instruments of credit.

Since those central bankers and virtually all empowered economists believe that money supply (as espoused by Modern Monetary Theory) and inflation are unconnected, and indeed that some arbitrary degree of inflation (2%) is necessary despite no historical precedents for same, they seek to cool the economy by raising their artificially created interest rates. Raising interest rates to reverse and restrict the effects of pouring gasoline on the embers of a partially drowned economy (first the credit debacle of 2008 and now the pandemic shutdown) does not really "withdraw" excess fake money or uncollateralized credit from the economy. Trying to dampen the wage-price spiral by decreasing consumers’ purchasing power will lead to unaffordable borrowing costs for businesses and higher unemployment.

Those businesses and unemployed persons will extinguish the excess money supply by using up savings (as we are seeing in the persistent consumer boom in the U.S. despite rising un-and under-employment)--an ‘Austrian economic’ exchange of diminishing value dollars for real goods) and extending further expansion of the fake money supply through use of credit until that gradually tightening source becomes too expensive. That will be followed by extinguishing credit and capital via recognized de facto bankruptcy. Unrecognized de facto bankruptcy is already present for many individuals and businesses who cover, bank-like, by "swaps" of credit through different sources, and in most banks and the Federal Reserve banks. The banks’ insolvency is cleverly hidden by accounting tricks kicking the can of real current market valuation down the road to maturity valuation. Those repayable dollars at maturity of course will be of markedly diminished purchasing power. Despite the Federal Reserve’s ‘tightening’, when comparing centrally bank interest rates to ‘real’ inflation (not the government’s carefully disguised CPI) those current interest rates are still negative; i.e. the largest borrowers are ‘paid’ to borrow.

This all derives from "our central bank <being> granted statutory freedom to set interest rates and inflation targets, an arrangement that has never delivered a functioning economy."

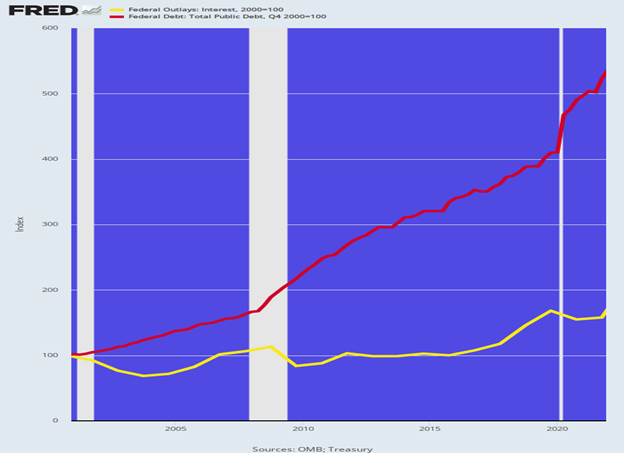

So presumably there is no reason for us to fret over governmental default, right"?Central to the U.S. debt-ceiling and budget debate is the often-repeated claim that negotiations must be concluded immediately to ensure that the US does not miss payments on any of its debts foreign or domestic. This is an out-and-out lie. The US has absolutely, indisputably defaulted before. This began in in the wake of the American Revolution when the US defaulted on domestic loans. After the new constitution was in place in 1790, the federal government renegotiated past debt at less favorable terms for investors. That's a default. The following chart from the St. Louis Fed shows where we are headed:

To paraphrase Emile Woolf and others: The real role of a central bank shoube to protect the national currency's purchasing power, leaving interest rates to the unimpeded market at large.

That can only happen when/if a fiat currency supply is no longer based on the full faith and credit of a government, but is fixed through direct backing (not necessarily exchangeable) by a non-perishable commodity such as gold, the supply of which is only slowly enlargeable through real, not digital, mining. Transient periods of increased money supply causing temporary inflation could be allowed, as has been done in the past, for financing warfare or extraordinary public works (think Panama Canal) as long as the resultant increase is deliberately and rapidly extinguished afterwards--perhaps an anachronistic fantasy. It has happened before, however. Witness the stability of the British pound's purchasing power, backed by gold, for over a century with mild blips during wartime.

Witness the funding of U.S. participation in WWI and WWII by government acquisition of private capital through selling war bonds and stamps. Imagine if our government had to seek popular approbation for endless foreign wars via that mechanism, instead of using Executive Orders, Congressional Resolutions, and limitless debt creation!

Fundamental reform would upset too many apple carts. Besides a massive revision in the mission of the Federal Reserve and our banking system, two other issues of international consequence come to mind. As

writes,"instituting tariff-free trade (regardless of reciprocation) enabling manufacturers to source materials and components from anywhere in the world."

Given that the U.S. has effectively done a version of this for many decades, and the (partially) free market has answered by exporting jobs and production overseas since the 1980’s for cheaper labor and resources, how are we to reverse our conversion from a consumptive economy which involutes to a productive economy of balanced services and capital creation? Will a restoration of stable purchasing power of a national non-fiat currency be attractive enough to reverse production flight?

This plus a return to energy independence might be enough, for domestic energy availability and production is the quintessential keystone of any economy. But we are pursuing the exact opposite of these two measures, and remain blinded to the rapid decay of our monetary system. How much longer will our and all Western dollar-based countries be able to conceal the fundamental bankruptcy of their economies through accounting smoke and mirrors, disinformation, and providing endless amounts of false valuations to the populace? This economic "circle jerk" is a whirlpool of descent. Their only hope of obscuring this vicious cycle is probably a Central Bank Digital Currency, wherein not only the value is artificially defined by the issuers without any market influence but also the use of same is completely centrally controlled. This must be the final recipe for "from each according to their means to each according to their needs". This is also the only means of realizing reparations for all definable victims and true equity for all.

The result will be that ascribed by Woolf:

"The alternative to fundamental reform is, of course, more of the same: punishing levels of debt, negative growth and eventual economic collapse.”

By our acquiescence in continuing this charade, we all are witnesses to a kind of economic murder, a domestic Dollaricide.

Surely we will be maintained by the internationally foundational state of the U.S. dollar? Or is the international paradigm rapidly shifting to new hemispheres and hegemonies? That is the subject of Dollaricide II.

To be continued….